Last Updated: 22 February 2026

Key Takeaways

- UPDATE: 22 February 2026

- GBP exchange rate is hovering around $1.35 to the pound. GBP has lost some of its strength, however GBP remains about 7% higher than a year ago

- The ISA/SIPP Rule: Prefer Accumulation (Acc) funds to automate compounding tax-free.

- The GIA Rule: Lean towards Distributing (Dist) funds to simplify tax reporting and avoid “notional distribution” admin.

- Currency Risk is Real: A strong Pound can eat your US stock gains and yield less than you expect. Use Pound-Cost Averaging to smooth out FX volatility.

- Check the Tracking: iShares often outperforms Vanguard in net returns due to more aggressive Securities Lending revenue.

- Zero-Fees: Use InvestEngine, Trading 212, or Freetrade to hold UK-listed ETFs with £0 platform or dealing fees.

In this Guide

What is an ETF – more specifically a UCITS ETF?

Managing a portfolio over the long term teaches you that complexity is often the enemy of consistent returns. For those of us focused on building a robust core without the noise, the Exchange Traded Fund (ETF) is the most efficient tool at our disposal. Essentially, an ETF is a “basket” of securities that tracks an index but trades on an exchange just like an individual stock. However, for a UK investor, the label “UCITS” is arguably more important than the ticker itself.

UCITS (Undertakings for Collective Investment in Transferable Securities) is the gold-standard European regulatory framework. It ensures the fund is well-diversified (preventing any single stock from over-dominating), liquid enough for you to exit at any time, and—crucially—that your assets are held by an independent custodian. If the fund provider fails, your underlying shares remain protected.

In this space, two titans dominate with a combined global market share of over 60%: iShares (BlackRock) and Vanguard. iShares is the larger of the two globally, commanding roughly 30+% of the market with a focus on liquidity and tactical variety. Vanguard, the “retail hero,” holds around 25% and is preferred by many UK investors for its low-cost, mutual-ownership philosophy. In the UK, you’ll find that staples like the Vanguard S&P 500 (VUSA/VUAG) and the FTSE All-World (VWRL/VWRP) are the bedrock of most portfolios, while iShares’ Core S&P 500 (CSP1) and Core FTSE 100 (ISF) are the go-to choices for those seeking maximum liquidity and tight tracking.

Why invest in an ETF and not individual shares?

After a lot of trial, error, and the occasional calculated risk, my conviction has settled firmly on the efficiency of ETF investing. Today, over 60% of my capital is held within Vanguard and iShares ETFs—a choice born not from a lack of ambition, but from a respect for market history.

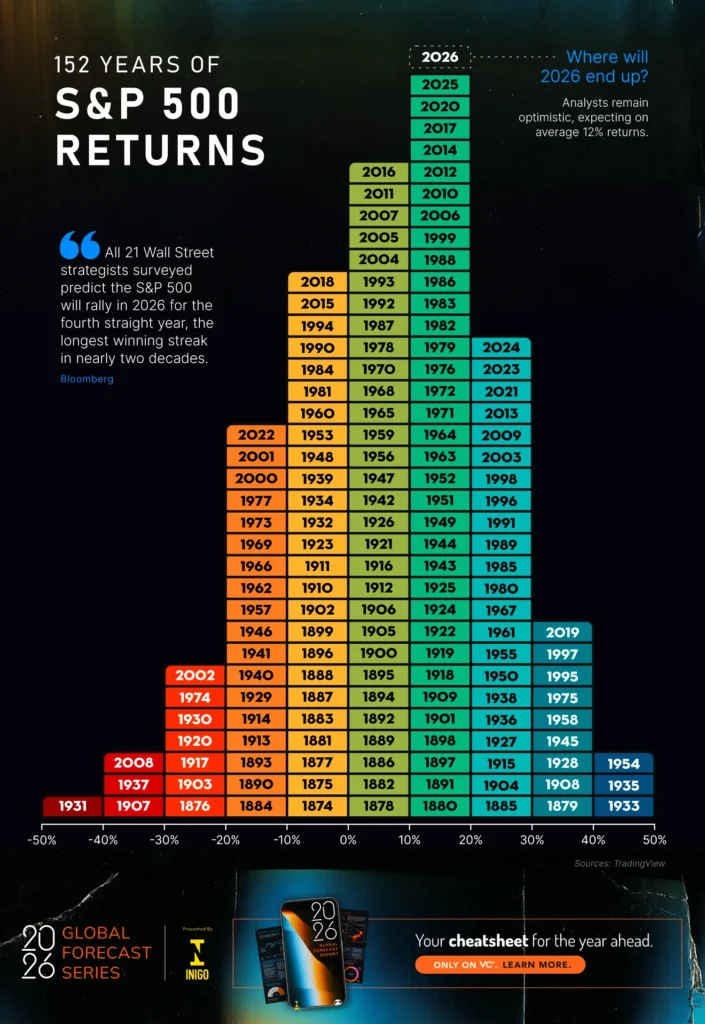

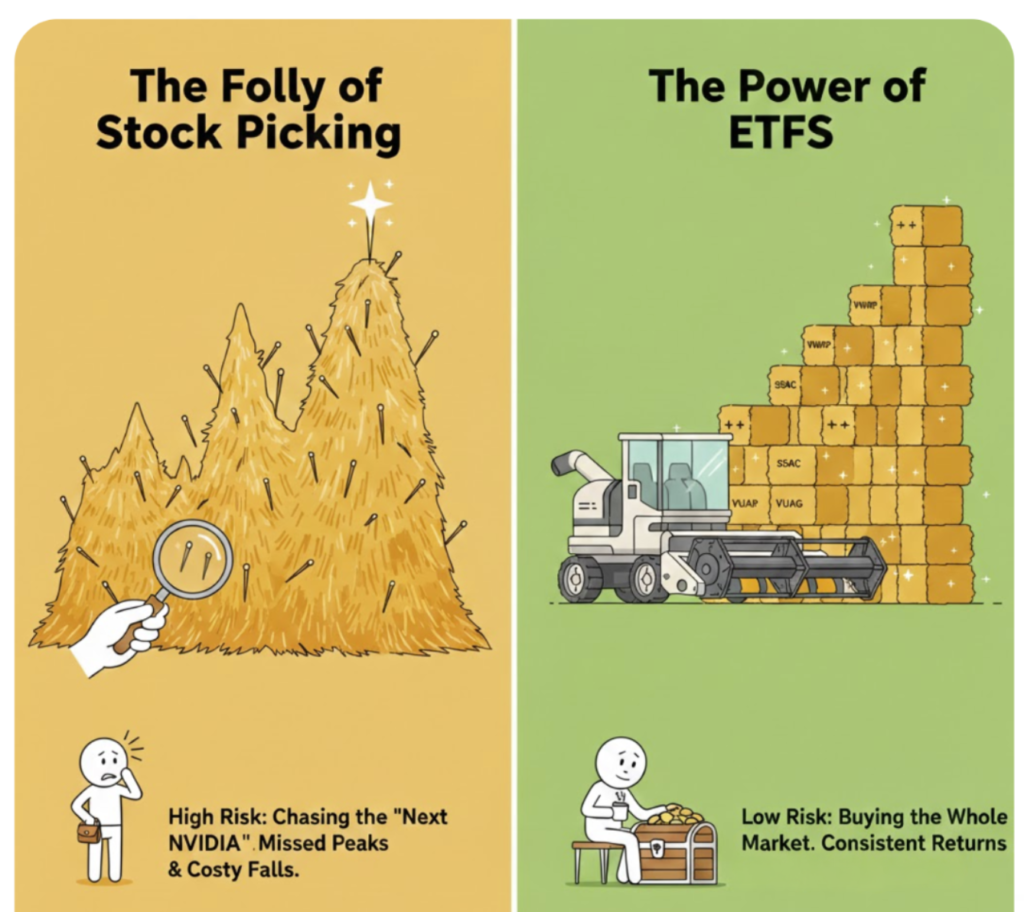

With the benefit of hindsight, those who backed NVIDIA or Microsoft a decade ago have seen returns that make “boring” index investing look pedestrian. However, the graveyard of individual stock picking is far more crowded. One need only look at the recent volatility of names like Snapchat or Oracle to see how quickly a “phenomenal” rise can turn into an even harder fall.

The reality is that for the vast majority of us, the most reliable path to wealth isn’t finding the needle in the haystack; it’s simply buying the whole haystack.

The logic for this approach is supported by more than just personal preference; the data is quite staggering. Year after year, SPIVA (S&P Indices Versus Active) scorecards show that upwards of 90% of professional fund managers fail to beat a simple index tracker over a ten-year period.

When you factor in the “professional” fees—often exceeding 1% per annum—versus the 0.07% to 0.10% charged by a low-cost ETF, the outcome is almost mathematically predetermined. For the average UK retail investor, the ETF offers a “set and forget” engine: steady, regular contributions into a diversified basket that ensures inflation-beating returns without the idiosyncratic risks that can be posed by picking individual shares.

In my experience, the peace of mind that comes with knowing you aren’t one bad CEO decision away from a 50% drawdown is worth far more than the thrill of a speculative bet. While my “core” is passive, I use the stability of these ETFs to provide the margin for more tactical plays elsewhere in my portfolio. It is this balance—the stability of the index paired with the experience to know when to take a calculated risk—that has allowed me to maintain a steady course through the market cycles of the last 20+ years.

The Ticker Table: Vanguard vs. iShares (2026 Edition)

Below is a breakdown of the most precise choices for a UK portfolio. Note how iShares often uses slightly different branding (like “Core”) for their flagship passive trackers. I personally hold a significant portion of my wealth in a mixture of VUSA, IUSA, VHYL, and VUKE across both my ISA and GIA. These are all Pound-priced (£) on the London Stock Exchange, meaning you don’t pay “hidden” FX conversion fees to your broker just to buy or sell them.

| Asset Class | Vanguard (Distributing) | Vanguard (Accumulating) | iShares (Distributing) | iShares (Accumulating) |

| S&P 500 | VUSA | VUAG | IUSA | CSP1 |

| FTSE All-World | VWRL | VWRP | — | SSAC |

| FTSE 100 | VUKE | VUKG | ISF | CUKX |

| FTSE 250 | VMID | VMIG | MIDD | — |

| Global Dividend | VHYL | VHYG | IWRD | IWDA |

A good explanation of the VUSA and VUAG ETFs is provided in the video below.

You can buy every one of these tickers on the major UK platforms, but the costs vary wildly. Having moved my own capital between these providers over the years, here is my view:

- Trading 212: The Low-Cost King. They offer £0 commission and £0 platform fees. Because the ETFs above are GBP denominated, you also bypass their 0.15% FX fee. It is ideal for the ISA.

- Interactive Brokers (IBKR): If you plan on making regular large purchases in US shares, IBKR is the platform of choice. To buy ETFs, their commissions are ultra-low (typically around £3–£5 for large UK trades).

- Hargreaves Lansdown (HL): The Legacy Giant. Recently, HL reduced their online dealing fees to £6.95, but their ISA platform fee for ETFs is increasing to a hefty £150 per year for larger portfolios.

Accumulation vs. Income: The Strategy

The Accumulation (Acc) Advantage: The Compounding Engine

In an Acc fund, dividends are never paid to your broker’s cash account. Instead, the fund manager reinvests them directly back into the fund’s Net Asset Value (NAV).

- Why use it: It is the ultimate “set and forget” tool. You avoid “cash drag” (money sitting uninvested) and you don’t pay transaction fees to buy more shares manually.

- The “Experience” Tip: If you are in the wealth-building phase—Acc is your best friend. It ensures that the “power of compounding” isn’t interrupted by your own inertia.

The Distributing (Dist) Case: Tactical Cash Flow

Dist funds pay cash dividends into your account (usually quarterly).

- Why use it: It’s ideal for those who need to draw an income (retirement) or—tactically—for investors who want to use dividend cash to fund a different part of their strategy.

What should I buy in my ISA and GIA?

The tax treatment differs significantly based on where the fund is “wrapped.”

- In your ISA (or SIPP): Always lean toward Accumulation (Acc). Since there is no tax on dividends or capital gains within an ISA, you want the most efficient compounding possible. You don’t want to manually reinvest dividends; let the fund manager do it for free.

- In your General Investment Account (GIA): Lean toward Distributing (Dist). HMRC taxes you on dividends even if they are “accumulated” inside the fund (notional distributions). If you hold Acc in a GIA, you must manually track these notional dividends and add them to your “cost basis” to avoid being double-taxed on Capital Gains when you sell. It is an administrative nightmare. With Dist funds, the cash hits your account, the tax statement is clear, and your cost basis remains simple.

A Word of Warning – The Risks!

From personal experience—watch out for concentration and currency risks! Even though ETF investing is lower risk than picking individual shares, there are critical issues to be aware of.

One of the most common pitfalls for UK investors is the “Home Bias” trap or its opposite, the “S&P 500 Tunnel Vision.” After a decade of watching US tech giants outpace almost everything else, it is tempting to go all-in on America. However, a methodical approach requires understanding that your returns are dictated by two things: the price of the shares and the strength of the currency you used to buy them.

Most seasoned portfolios use a mix of these three regional exposures:

- US ETFs (S&P 500): The engine of growth. You are buying the most innovative companies on earth.

- UK ETFs (FTSE 100/250): The value and yield play. UK markets are often “cheaper” and offer higher dividends.

- Global ETFs (All-World): The “Safety Net.” This captures the rise of emerging giants and ensures you aren’t wiped out if one economy falters.

The Concentration Trap: Is “Global” actually US?

A major “dirty secret” of global investing in 2026 is that a Global ETF is actually about 62–65% US stocks.

If you hold both an S&P 500 ETF and a Global ETF, you aren’t just “diversifying”—you are doubling down on America. In the S&P 500, the “Magnificent Seven” (Apple, Microsoft, NVIDIA, etc.) now account for roughly 33% of the entire index. If just seven companies dictate 1/3rd of your “diversified” fund, you aren’t as diversified as you think.

Note: If just seven companies dictate 1/3rd of your “diversified” fund, you aren’t as diversified as you think. A bad quarter for one chipmaker or software giant can now move the entire market.

Currency Risk

Just because some of these ETFs like VUSA or IUSA are priced in £, doesn’t mean they are currency risk-free. When you buy a US ETF like VUSA, you are effectively selling Pounds to buy Dollars.

The “Weak Pound” Scenario: Imagine you bought VUSA when the Pound was weak (£1 = $1.25). If the S&P 500 rises by 15%, but the Pound then strengthens to $1.35, the currency move eats your gains.

- S&P 500 gain: +15%

- Currency “drag”: -7%

- Your Realised Return: +8%

This is why I advocate for Pound-Cost Averaging. By drip-feeding money into these ETFs monthly, you aren’t just averaging the price of the stocks; you are also averaging the exchange rate.

Don’t be afraid of US exposure—it’s the world’s most powerful economic engine—but respect the concentration. In my portfolio, I balance my heavy US holdings with some UK funds. This keeps my base currency (Sterling) represented and provides a buffer when the Dollar takes a dive. There are more complex “currency hedged” versions of some of these ETFs – but I tend to find their performance lower and fees higher – so I personally accept the currency risk as a cost of doing business.

Tracking Difference: Why iShares often beats Vanguard

When picking an ETF, most people look at the fee (OCF). I’ve learned that the Tracking Difference (TD) is the true cost of ownership. Take a look here – the differences are small but can be significant when compounded over a number of years!

Tracking Difference is the actual gap between the index’s return and what you get in your account. Ideally, it should be as close to zero as possible. However, in the 2024–2026 period, we’ve seen a fascinating trend: iShares often has a better (smaller) tracking difference than Vanguard, despite having similar fees.

The reason? Securities Lending. iShares (BlackRock) is very efficient at lending out the shares within the ETF to short-sellers. They pass a large chunk of that revenue back into the fund, which effectively “offsets” the management fee. In some years, this has actually resulted in iShares funds outperforming the index they are supposed to track. This is something I have only realised recently – and I will be spending 2026 switching out of some of my Vanguard funds and rotating them into iShares!

| Asset Class | Vanguard Ticker | iShares Ticker | Why iShares can win here |

| S&P 500 | VUAG | CSP1 | CSP1 has massive Assets Under Management (£80bn+), giving it better “lending alpha.” |

| All-World | VWRP | SSAC | iShares uses “Sampling” (buying the best stocks) rather than Vanguard’s “Full Replication.” |

| FTSE 100 | VUKG | CUKX | CUKX tracks the index more tightly during volatile UK periods. |

Recommendation: Build Your Own ETF Portfolio

Choosing your allocation is a personal decision based on your risk tolerance. I’ve found that these three “Profiles” cover most UK retail needs.

| Strategy Profile | Suggested Mix | Why choose this? |

| US Tilt | Vanguard: 70% VUAG / 30% VMIG or VUKG iShares: 70% CSP1 / 30% MIDX or CUKX | High exposure to US Tech/AI via the S&P 500, balanced with UK growth. |

| Global | Vanguard: 100% VWRP iShares: 100% SSAC | You just want the global average. BUT – Global still has ~ 60%+ US exposure! |

| Income – Balanced | Vanguard: 50% VWRP / 30% VHYL / 20% VUKE iShares: 50% SSAC / 30% IWRD / 20% ISF | Global growth balanced with high-dividend yield and stable UK “Blue Chips.” |

Investing is about being disciplined. Pick a strategy, understand the currency and concentration risks, and let the compounding and time do the heavy lifting while you get on with your life.

How to Buy These ETFs for £0 Fees

If your goal is to buy the £-priced tickers (like VUSA or VWRP) and hold them long-term, these three platforms are currently the only ones offering a truly commission-free and platform-fee-free experience. More information on a platform review is provided here.

| Platform | Dealing Fee | Annual Platform Fee | Best For… |

| InvestEngine | £0 | £0 (DIY Portfolio) | The ETF Specialist. It is arguably the cheapest way to build a diversified portfolio. No ISA fees, no SIPP fees, and a dedicated focus on ETFs. |

| Trading 212 | £0 | £0 | The All-Rounder. Excellent for “Pies” (automated investing) and their ISA is completely free. Plus, they pay competitive interest on your uninvested cash. |

| Freetrade | £0 | £0 (Basic Plan) | The Simple Choice. Their “Basic” plan is free for GIAs and ISAs, though you’ll need their “Plus” tier (£11.99/mo) if you want the SIPP or interest on larger cash balances. |

Why are there no fees? If you plan to do more than just buy GBP denominated ETFs e.g. US/UK shares see my other guide

- Priced in £: Because you are buying UK-listed ETFs in Pounds, you bypass the FX fees that these platforms usually charge for US stocks (like the 0.15% at T212 or 0.99% at Freetrade).

- Share Lending: Most free platforms (and even some paid ones like HL) earn revenue by lending out your shares to institutional “short sellers.” This is standard practice, but it’s why they can afford to waive your fees.