Last Updated: 20 February 2026

Key Takeaways

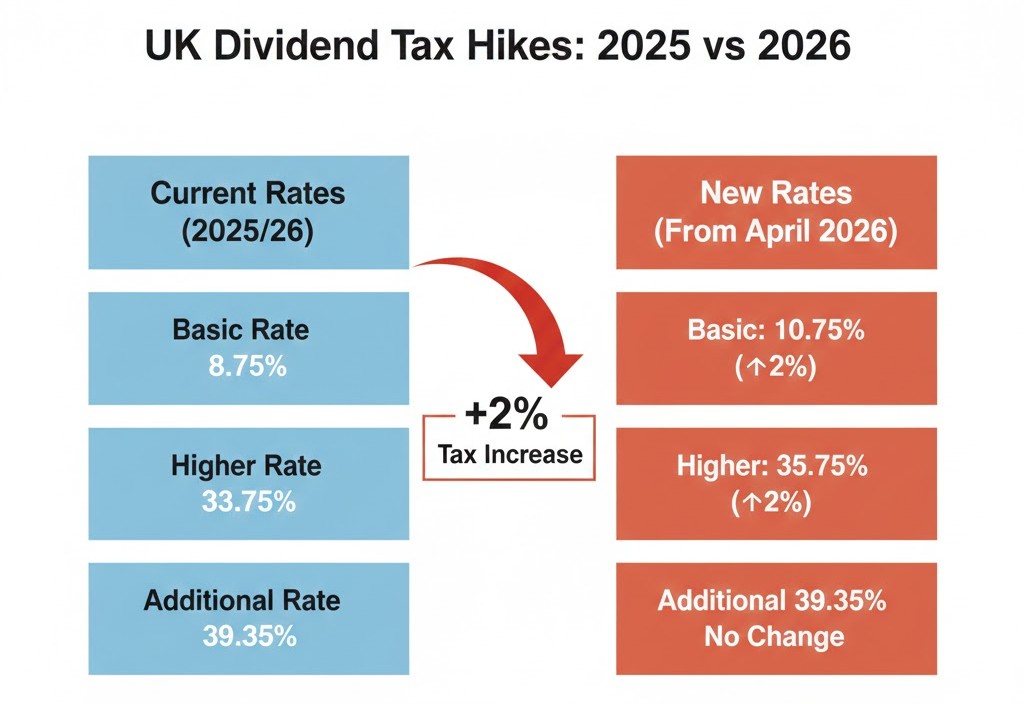

- The 2% Hike: From April 6, 2026, dividend tax rates rise to 10.75% (Basic) and 35.75% (Higher). Every £1,000 in dividends now costs you more—act before the deadline.

- CGT: Main rates have shifted to 18% (Basic) and 24% (Higher). The allowance is frozen at a tiny £3,000.

- Tax-Loss Harvesting (Critical): Use your “losers” to pay for your “winners.” Sell underperforming stocks in your GIA to offset gains. You can carry unused losses forward indefinitely, but you must claim them within 4 years

- The “Bed & ISA” Loophole: Bypass the 30-day “wash sale” rule by selling in your GIA and rebuying immediately inside an ISA or SIPP. This resets your cost basis and shelters all future growth.

- Low Coupon Gilts (e.g. T26A & TN28): These act as a “shadow ISA” once your £20k limit is hit. They provide tax-free capital gains that ignore the Personal Savings Allowance.

- The (Proposed) 2027 Cliff: Prepare for the £12,000 Cash ISA cap by mastering Gilts now. High-net-worth savers who wait until 2027 to learn this will face a massive tax bill.

- Premium Bonds: Only viable for emergency funds if you hold £22k+ to “force” the probabilities in your favor. If you hold less than £22,000, your median expected return drops significantly—for many, the most likely annual return is 0%, making it a poor choice compared to a tax-free Gilt

In this Guide

If you thought the tax landscape for UK investors was already tight, April 6th, 2026, is about to be a wake-up call. The Chancellor has confirmed a 2% increase in dividend tax rates for Basic and Higher rate taxpayers.

With the dividend allowance frozen at a measly £500, HMRC is effectively coming for your “passive” income. If you don’t optimise your portfolio now, you are essentially leaving 2% of your hard-earned yield on the table.

What the 2% Dividend Tax Hike Costs You

The shift is subtle but expensive. Here is how the bands are changing. For a Higher Rate taxpayer with £10,000 in dividends, this hike—combined with the tiny allowance—means an extra £190 per year goes to HMRC instead of your retirement fund. Over a decade of compounding, that is a five-figure mistake.

| Tax Band | Current Rate (2025/26) | New Rate (From April 2026) |

| Basic Rate | 8.75% | 10.75% |

| Higher Rate | 33.75% | 35.75% |

| Additional Rate | 39.35% | 39.35% |

The ISA vs. GIA Choice

One of the biggest mistakes investors make is treating their ISA and General Investment Account (GIA) as identical. They aren’t. To minimise tax leakage in the 2026 landscape, you need a “Yield vs. Growth” hierarchy:

- Priority 1: High-Yielders in the ISA. Any stock with a high dividend (think UK Banks, Miners, or Tobacco) should be shielded in your ISA. With the Higher Rate dividend tax now at 35.75%, the “dividend drag” on your wealth is at an all-time high. Because dividends are taxed as income every time they pay out, the hit is immediate and compound-killing.

- Priority 2: Growth Stocks in the GIA. Low-yield or non-dividend payers (like US Tech or Small-Caps) are better suited for your GIA. Why? Because the main Capital Gains Tax rates have jumped to 18% (Basic) and 24% (Higher). However, unlike dividends, CGT is only triggered when you sell.

- The “Safety Net”: Tax-Loss Harvesting. The GIA has one hidden advantage over the ISA: you can use losses to your benefit. If a position drops, selling it allows you to “bank” that loss to offset future gains. Crucially, you have exactly 4 years from the end of the tax year in which you made the loss to report it to HMRC. Once reported, these losses can be carried forward indefinitely, acting as a “tax shield” for when your growth stocks eventually take off.

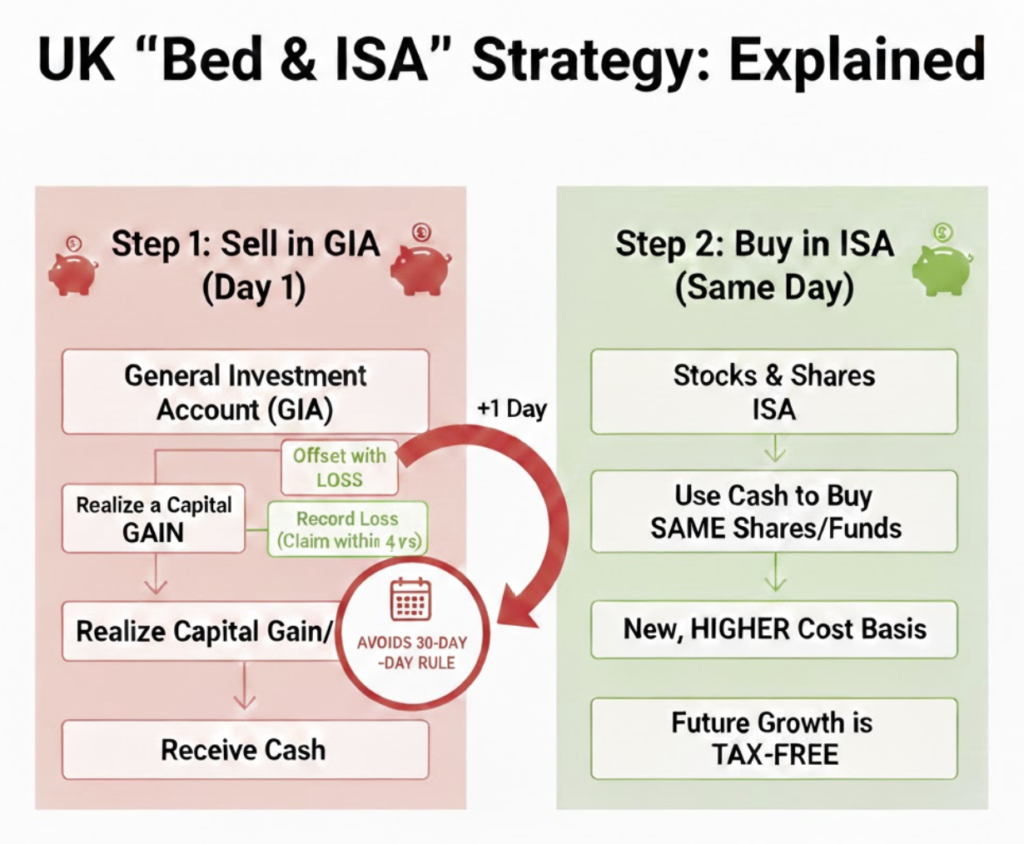

The “Bed & ISA” & The 30-Day Rule

The most effective way to “fix” a tax-heavy GIA is the Bed & ISA maneuver: selling your shares and immediately rebuying them within the ISA.

Watch the “Share Matching Rules”: also known as the 30-day rule.

- If you sell shares for a loss in your GIA and buy them back in the same GIA within 30 days, HMRC “matches” the old price to the new one, essentially cancelling out your tax loss.

- The Loophole: Buying them back inside an ISA or SIPP does not trigger the 30-day rule. You effectively reset your cost base and shelter all future dividends in one move.

Harvesting Losses to Minimise your Tax Liability

If you’ve cashed in shares recently and are staring down a big Capital Gains Tax bill, look for the “red” in your GIA portfolio. Selling stocks that are currently at a loss—even if you still believe in them—can be used to offset your gains. This is Tax-Loss Harvesting. Remember – you can buy the shares back inside an ISA or SIPP soon after selling your shares at a loss in the GIA. This is a very powerful loophole that can be used in your favour.

Sell the loser (or part of the losing position), use the loss to wipe out your tax bill, and then wait 31 days to rebuy (or rebuy immediately in your ISA) to stay “in the market” without the tax liability.

Defeating the “Personal Savings Allowance” Trap

While the dividend hike is getting the headlines, a silent tax is eating away at cash savers. With interest rates sitting around 3.75% – 4.5%, it is incredibly easy to hit your Personal Savings Allowance (PSA):

- Basic Rate Taxpayers: £1,000 annual limit. (Exceeded with just £23,000 in a 4.5% account).

- Higher Rate Taxpayers: £500 annual limit. (Exceeded with just £11,500 in a 4.5% account).

- Additional Rate Taxpayers: £0 allowance.

If you are a Higher Rate taxpayer with £30,000 in a standard savings account, you aren’t earning 4.5%. After tax, your “real” return on the bulk of that cash is a disappointing 2.7%.

The “Gilt” Strategy: Your Tax Free Interest Alternative

A Gilt is simply an IOU from the UK Government. When you “buy” a gilt, you are lending the government money for a fixed period. In return, they pay you a tiny amount of interest (the coupon) and a guarantee to pay back exactly £100 per share at the end (the maturity). A mixture of investing in Gilts and ETFs is not an uncommon strategy.

For example, take the T26A gilt (0.375% Treasury Gilt 2026). As of early 2026, you can buy this for roughly £98.05. On 22 October 2026, the government will pay you £100 for every share you own.

- The Profit: You make £1.95 per share.

- The Tax Loophole: While the 0.375% interest is taxable, that £1.95 capital gain is 100% tax-free. Because this gain makes up the bulk of your return, your “real” tax rate is practically zero.

One attractive solution to minimise paying taxes is to invest in low coupon Gilts like T26A (0.375% 2026) and TN28 (0.125% 2028). The key words here are “low coupon”!

Why low coupon? Gilts have a unique tax superpower: while the tiny “coupon” (interest) is taxable, the Capital Gain is 100% tax-free. By buying a Gilt priced at £98 that matures at £100, that £2 gain is yours to keep, even if you’ve exhausted all other allowances.

Gilts vs. High Street Bank Accounts

For those with significant cash to “park,” the traditional bank account has become a tax liability. As interest rates remain high, the Personal Savings Allowance (PSA) is being obliterated.

If you are a Higher Rate taxpayer, you only get £500 of tax-free interest. If you are an Additional Rate taxpayer, you get £0.

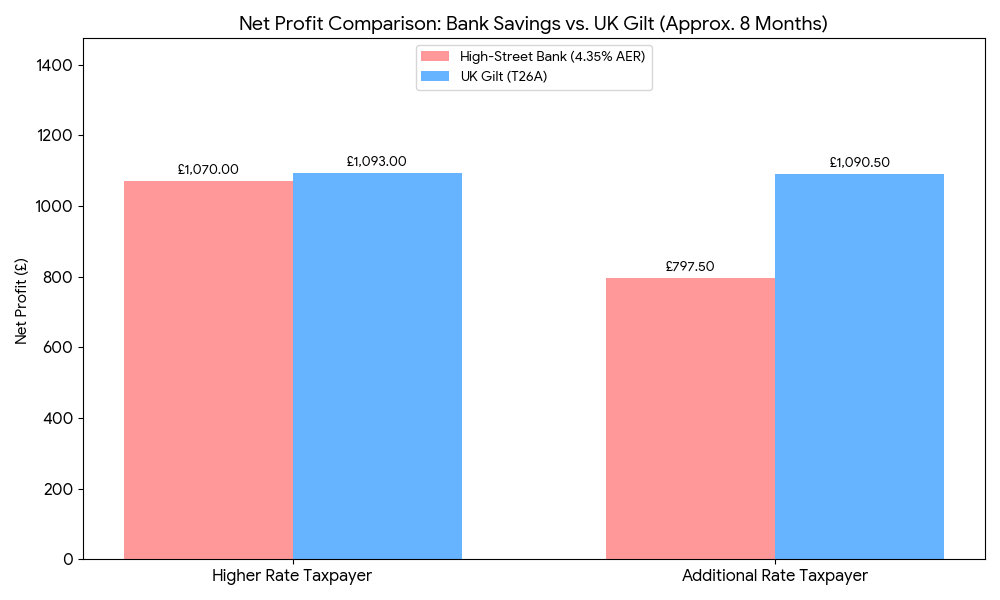

£50,000 Cash Comparison (Higher vs. Additional Rate)

If you have £50,000 to invest for roughly 8 months, here is how the 2026 tax landscape treats a high-yield bank account versus a short-term Gilt like T26A. You think you might earn more from a higher yielding savings account – but for higher and especially additional rate tax payers – the low coupon gilt wins hands down.

| Feature | High-Street Bank (4.35%) – 8 month return | UK Gilt (T26A) – 8 month return |

| Gross Return | £1,450.00 | £1,113.00 |

| Tax Treatment | Taxed as Interest | Capital Gains Exempt |

| Annual Allowance | £500 (Higher) / £0 (Add.) | Unlimited (Gains) |

The Verdict: For an Additional Rate taxpayer, the bank account is a disaster. You lose nearly half your profit to HMRC. By using a Gilt, you keep over £290 more of your own money on a £50k investment because the £1.95 per share gain (from £98.05 to £100) is 100% tax-free. For an Additional Rate taxpayer, the goal is to find Gilts with the lowest possible coupon. This ensures the majority of your return comes from the tax-free capital gain rather than the taxable interest payment.

| Gilt Ticker | Maturity Date | Coupon Rate | Clean Price (per £100) | Annualized Capital Gain (Tax-Free) |

| T26A | 22 Oct 2026 | 0.375% | £98.05 | ~2.93% |

| TG27 | 22 July 2027 | 1.250% | £96.91 | ~2.18% |

| TN28 | 31 Jan 2028 | 0.125% | £93.93 | ~3.27% |

Why buy Gilts instead of just using an ISA?

While the ISA is the “Gold Standard,” Gilts are becoming the essential secondary tool for three reasons:

- Exceeding the Limit: Once your £20k annual ISA limit is gone, Gilts offer a “shadow ISA” for your remaining cash with no upper limit on the tax-free capital gains.

- Strategic Shielding: Sophisticated investors prefer to save their ISA “space” for high-growth shares or high-yield dividends, using the Gilt market to handle their safe, “boring” cash management.

- The 2027 Cliff: From April 2027, the government is capping Cash ISA contributions at £12,000 for those under 65. Learning the Gilt market now is no longer optional; it is a necessary skill for anyone looking to shelter cash from 2027 onwards.

⚠️ A Word of Warning: Risk and Liquidity

- While Gilts are backed by the UK Government, they are not “static” savings accounts. They are tradable instruments, and their market price moves every day.

- The “Maturity Guarantee”: If you buy T26A or TN28 and hold them until their respective maturity dates, you are guaranteed to receive £100 per share. The risk of losing your principal is virtually zero if you wait for the government to pay you back.

- The “Early Exit” Risk: If you need to sell your Gilts before they mature, you are at the mercy of the market price.

- T26A (Short Term): Because it matures in late 2026, its price is very stable. Even if interest rates rise, its price won’t fluctuate much because the “finish line” is so close.

- TN28 (Medium Term): This Gilt is more sensitive. Because it has roughly two years left, a sudden spike in UK interest rates could cause its market price to drop below what you paid. If you are forced to sell during that dip, you could get back less than you invested.

- The Rule of Thumb: Only invest in Gilts where the maturity date aligns with when you actually need the cash. If there is a chance you need the money “tomorrow,” stick to the ultra-short T26A or a standard instant-access account.

Where to Buy Gilts

To execute this strategy, you need a broker that gives you direct access to the London Stock Exchange (LSE) gilt desk:

- Interactive Brokers (IBKR): A top choice for the lowest fees (roughly 0.1% commission). It’s powerful and cheap, but the interface is professional-grade and can be intimidating for beginners.

- AJ Bell: The best “middle ground” for most UK investors. It offers a much simpler, user-friendly interface than IBKR but with significantly lower fees than the traditional “big” brokers.

- Hargreaves Lansdown (HL): Very easy to use and excellent customer service, but their trading fees (up to £11.95 per trade) can eat into the narrow profit margins of a Gilt strategy unless you are trading very large sums.

A comparison of the merits of each broker is provided here. Note: You cannot buy Gilts with Trading 212.

Premium Bonds—The £22,000 “Secret”

If you want 100% tax-free returns with instant access, Premium Bonds are the classic choice. However, most people play the game wrong.

The odds of winning any prize are currently 22,000 to 1. This leads to a mathematical reality:

The £22k Rule: To have a statistically “reliable” chance of winning at least one £25 prize every single month, you need to hold at least £22,000 in bonds.

If you have £1,000 in Premium Bonds, you are essentially in a lottery where you will likely win nothing for years. While Premium Bonds offer safety, tax‑free prizes, and the thrill of a lottery, the expected financial return for most people is low—often 0% in a typical year unless you hold a large amount. The government benefits significantly because Premium Bonds are effectively a cheap loan from savers, with many people earning less than the advertised average return. The video compares Premium Bonds with savings accounts, ISAs, and gilts, concluding that Premium Bonds can make sense for fun or for tax‑free parking of cash once other allowances are used, but they are not a wealth‑building tool. For longer term wealth building investing in gold may be a more lucrative higher yielding option.

Conclusion

The era of “lazy” investing is over. With the 2026 tax hikes targeting basic and higher-rate taxpayers alike, your portfolio must be more than just diversified—it must be tax-surgical.

A winning 2026 strategy relies on three distinct pillars:

- The Shield (ISA): Use this for your highest-yielding assets. If an investment pays a chunky dividend or has massive growth potential, it belongs here. Period.

- The Engine (GIA): Treat your GIA as a tool for “Tax Loss Harvesting.” By strategically selling losing positions to offset gains (and claiming those losses within the 4-year HMRC window), you can effectively “clean” your future profits.

- The Safe Haven (Gilts & Premium Bonds): For your “heavy lifting” cash—your emergency funds and house deposits—stop letting high-street banks take 40% of your interest. Low coupon Gilts (like T26A) and Premium Bonds provide the same security with a significantly higher net take-home pay.