Last Updated: 22 Feb 2026

Key Takeaways

- UPDATE: 22 February 2026

- The March 1st “HL Deadline”: You have 7 days left before Hargreaves Lansdown triples its ISA fee cap to £150. Large share/ETF holders should act now.

- Short on time? Jump to the 2026 Winner Verdict ↓

- Cheapest All-Rounder: Trading 212 remains the king of low-cost investing with £0 commissions and no monthly ISA fees.

- Best for US Shares: Interactive Brokers (IBKR) is unbeatable for large US trades due to its near-wholesale 0.03% FX fee.

- Simplicity Specialist: Freetrade has become a top-tier contender in 2026 by offering a £0/month ISA and SIPP on its Basic plan—perfect for UK-based “buy and hold” investors.

- Passive Investing King: Use InvestEngine for 0% fee “Set and Forget” index fund portfolios. It is currently the cheapest way in the UK to manage a DIY ETF portfolio.

- Crucial 2026 Update: Hargreaves Lansdown (HL) has tripled its share ISA fee cap from £45 to £150. Large portfolio holders should recalculate their costs immediately.

- Top Priority: Always complete your W-8BEN form to stop the IRS from taking 30% of your US dividends.

In this Guide

Choosing an investment platform in 2026 is no longer just about a slick app interface. From April 6, 2026, the basic dividend tax rate rises from 8.75% to 10.75%, and the higher rate to 35.75%. Along with the continued freeze on tax thresholds, your platform’s “hidden” costs—specifically Foreign Exchange (FX) fees—are now coming sharply into focus, and can become a primary drain on your wealth. Whether you are building a “set-and-forget” ETF portfolio or hunting for the next 10x US tech giant, here is the objective 2026 breakdown of where to put your money.

Investment Platform Comparison: 2026 Fees

In 2026, the market has split into “Fee Killers,” “Global Professionals,” and “Legacy Giants.” Note the major February/March 2026 fee overhauls for ii and HL below.

| Platform | Annual Account Fee | UK Share/ETF Trade | US Share/ETF Trade | FX Fee (Foreign Assets) |

| Trading 212 | £0 | £0 | £0 | 0.15% |

| InvestEngine | £0 | £0 (ETFs Only) | N/A | N/A |

| Freetrade (Basic) | £0 | £0 | £0 | 0.99% |

| Interactive Brokers | *£36 (£3/mo) | £3.00 | Min $0.35 ($0.0035 per share, capped at 1% of trade value) | 0.03% |

| AJ Bell | 0.25% (Capped at £42/year) | £5.00 | £5.00 | 0.75% |

| Hargreaves Lansdown | 0.35% (Capped to £150/year)** | £6.95 | £6.95 | 1.00%*** |

| Interactive Investor | £72 (£5.99/mo)**** | £3.99 | £3.99 | 0.75% |

**Effective March 1, 2026, HL has tripled the ISA platform fee cap for shares and ETFs from £45 to £150 per year for the ISA/SIPP. While the percentage fee dropped from 0.45% to 0.35%, this higher cap means most ISA investors with £43k+ in shares will actually pay more than they did in 2025

**Hargreaves Lansdown FX fees are tiered – 1.00% on the first £5000, 0.75% for the next £5000, 0.50% for the next £10000 and then 0.25% for the portion of the trade over £20000 – they remain some of the highest in the market

****For ii, their Core plan fee applies for portfolios up to £100,000.

The US Share Specialist: Interactive Brokers (IBKR)

If you are strictly buying US giants like Nvidia, Apple, or Tesla, Interactive Brokers is the mathematically superior choice. For a deeper dive on buying US shares, click here.

- The 0.03% FX Miracle: While most brokers charge 0.15% to 1.00%, IBKR charges a near-wholesale rate of 0.03%. On a £10,000 trade, you pay just £3 in FX fees, compared to £100 at Hargreaves Lansdown.

- Deep Access: You get access to thousands of US stocks and complex instruments that “lifestyle” apps don’t offer.

⚠️ Why IBKR is NOT for the “Mixed” Investor

Despite being the cheapest for US shares, IBKR can be more expensive for a mixed portfolio of UK shares and ETFs:

- The UK Surcharge: IBKR charges a minimum of £3.00 for every UK share or ETF trade. Compare this to Trading 212, where the same trade is £0.

- The Monthly “Rent”: IBKR charges a £3 monthly activity fee for ISAs. If you only trade once every few months, you are paying £36 a year just to hold the account.

- Complexity: The platform is designed for professionals. If you just want to buy £50 of the S&P 500 every month, the interface will feel like a cockpit of a Boeing 747.

The Simplicity Specialists: Freetrade & InvestEngine

While Trading 212 wins on raw features, Freetrade and InvestEngine have become the “go to” choices for 2026 investors who value a clean, distraction-free interface.

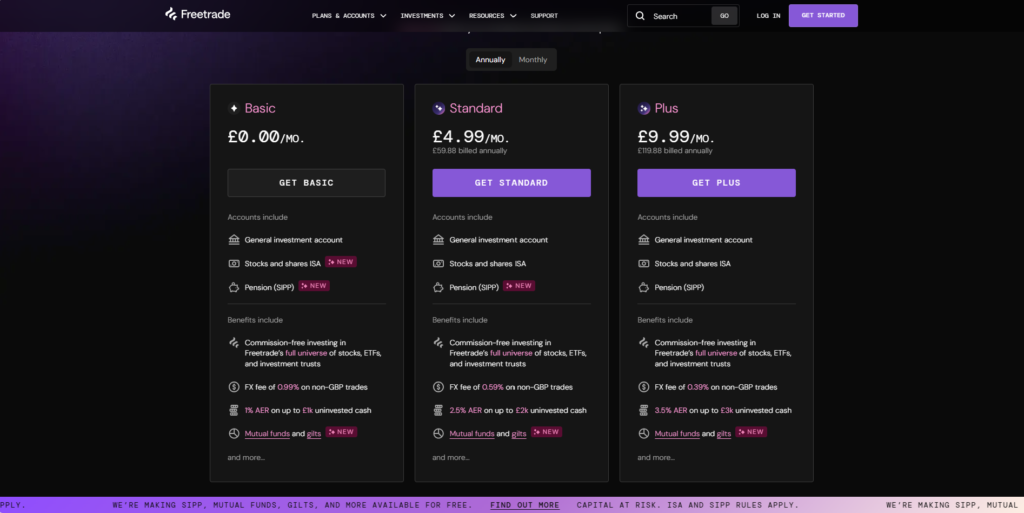

Freetrade: The All-Rounder

Freetrade reclaimed its “Beginner’s Choice” title in early 2026 by moving its ISA and SIPP onto the “Basic” plan for £0/month. This is a game-changer for those who want to buy UK-listed ETFs (like Vanguard’s VUSA) or individual UK stocks entirely for free.

- The Catch: If you venture into US stocks, the 0.99% FX fee on the free tier is steep. It’s a brilliant “buy and hold” home for your UK assets, but active US traders will find better options elsewhere

InvestEngine: The ETF Specialist

If you have zero interest in individual stocks and just want to build a ETF portfolio, InvestEngine is unbeatable. They charge £0 platform fees for DIY portfolios and offer advanced tools like “One-Click Rebalancing” and fractional ETFs—something even Freetrade currently lacks. InvestEngine is the top choice for passive ETF specialists.

- The Catch: You can only buy ETFs. There are no individual shares or investment trusts here. It is a specialist tool for a specialist job.

The All-Rounder Winner: Trading 212

For the average UK investor who wants a mix of UK shares, US shares, and ETFs, Trading 212 is currently unbeatable on price. Trading 212 dominates in 2026 by offering a completely free Stocks and Shares ISA alongside a market-leading 3.60% AER on its flexible Cash ISA. With £0 commissions, a 0.15% FX fee, and enhanced FSCS protection of up to £120,000 for cash deposits, it provides the best balance of value, safety, and ease of use for the majority of UK investors. You can even buy Bitcoin ETNs – check out my latest guide on the 2026 Bitcoin ISA deadline.

No Monthly Fees: Unlike IBKR or ii, there is no “account rent.” It is a 100% free ISA.

True Zero Commission: You pay £0 to buy UK-listed ETFs (like VUSA) or UK shares.

The Fractional Advantage: In early 2026, Eli Lilly (LLY) trades at over $1,000 (£830). On traditional platforms (HL/ii), you can’t buy £100 of it—you must buy a full share or nothing. On T212, you can buy exactly £100 (0.12 shares).

Understanding ETFs Across Platforms

You can buy ETFs on almost every platform mentioned, but the type of ETF changes the cost:

- GBP-Listed ETFs (e.g., VUSA): These trade in Pounds. You should buy these on Trading 212 or InvestEngine to avoid all commissions and FX fees.

- US-Listed ETFs: Due to UK regulations (UCITS), you generally cannot buy “pure” US ETFs like VOO. You must buy the UK-reporting equivalent (e.g., VUSA tracks the same S&P 500 index).

The “Consolidator” Strategy: ii & HL

If you have a large portfolio, the percentage-based fees of small apps start to matter less than the “Service” and “Wrappers” of the giants.

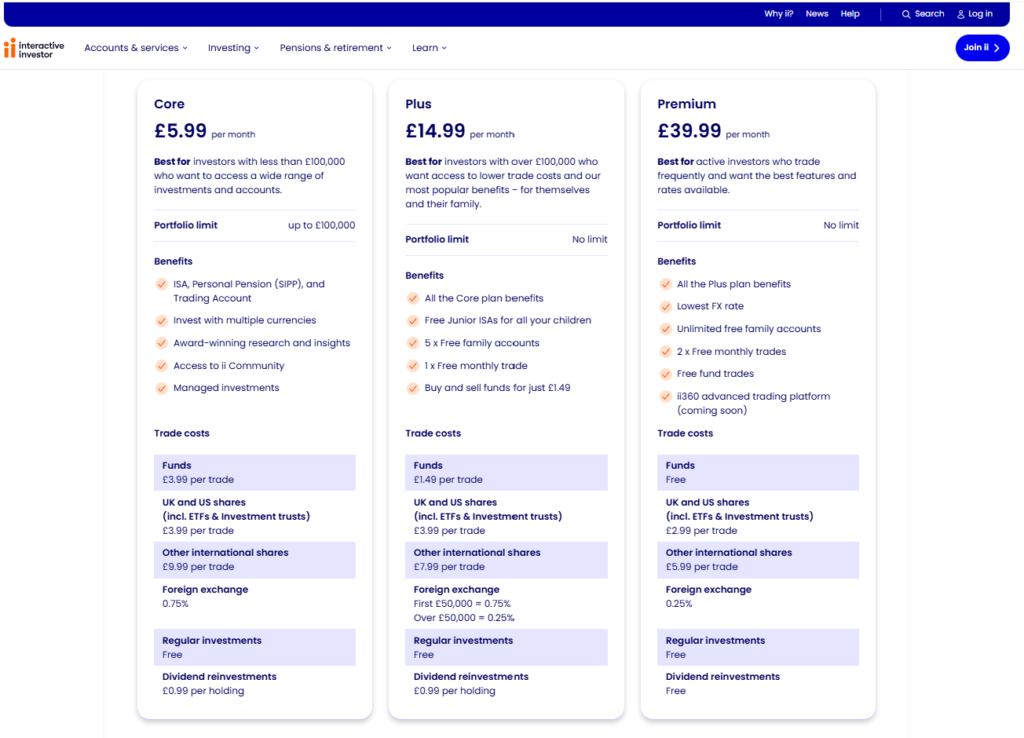

Interactive Investor (ii):

- Their new Core Plan (£5.99/mo) bundles your ISA, SIPP, and Trading Account under one single flat fee. It also allows you to hold USD in a “Multi-Currency Pot”. This means you convert Pounds to Dollars once, and then trade US stocks for free inside that USD pot thereafter. On percentage-based platforms (like HL or AJ Bell), a £250k pot would cost you £600–£1,000+ a year; with ii, it stays a flat £179.88.

- Unique for 2026, the Plus plan includes unlimited free Junior ISAs and allows you to add up to 5 family members for free. You can essentially run your entire household’s wealth through one subscription, saving hundreds in individual account fees.

- Institutional Asset Access: Unlike “app-only” brokers, ii provides access to 40,000+ instruments, including complex Investment Trusts, VCTs, and Corporate Bonds that seasoned investors use to protect capital during market volatility.

- Currency Flexibility: You can hold and trade in 9 different currencies. This is the “secret sauce” for large portfolios; by keeping your US Dividends in a USD sub-account, you avoid the constant 0.15%–1.0% “FX drag” every time you buy or sell.

Hargreaves Lansdown (HL): The premium choice for customer service. While their 1.00% FX fee is high, their SIPP (Pension) and LISA wrappers are robust and highly regulated.

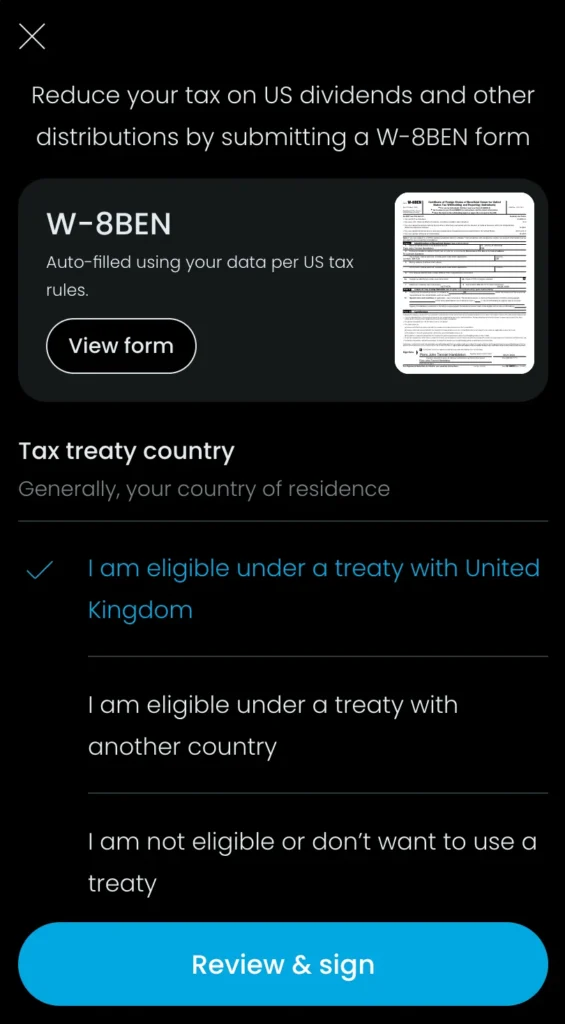

The 60-Second W-8BEN (Your Dividend Protector)

Regardless of your platform, if you own US shares, you must sign a W-8BEN form.

- The Saving: It reduces US withholding tax on your dividends from 30% to 15%.

- The Renewal: It expires every 3 years. Most apps like T212 handle this digitally in seconds. Do not skip it, or you are handing 15% of your profit back to the IRS.

Verdict: Who Wins for You?

- Strictly US Shares: Interactive Brokers (Cheapest 0.03% FX). I personally use IBKR for a core group of US shares that I trade frequently. For me, the savings add up to a few hundred pounds per year compared to Trading 212 due to the near-wholesale FX rates. Be warned: the interface is a ‘Boeing 747 cockpit’—it requires a lot of patience to master.

- Mixed UK, US, and ETFs: Trading 212 (Zero commission + No monthly fee). I hold both my ISA and GIA with Trading 212. While some recent app updates have been irksome, the platform remains the most intuitive on the market. Tip: the in-app share chats are great, but never treat a ‘Buy’ or ‘Sell’ post as a recommendation. Always do your own research.

- The Simplicity Winner: Freetrade (Ideal for beginners wanting a £0 ISA or SIPP to hold UK stocks and ETFs). I am in the process of transferring a SIPP of min held in HL to Freetrade to save on annual fees!

- Set and Forget Index Funds: InvestEngine (Unbeatable £0 fee for DIY ETF portfolios).

- Large Portfolios (£100k+): Interactive Investor. The Plus Plan (£14.99/mo) stops “cost creep” by bundling your ISA, SIPP, and Trading Account into one fee.

- The 2026 Edge: It includes free Junior ISAs for all your children and allows you to add 5 family members to your plan for free. You can also hold 9 different currencies, allowing you to buy US shares without losing money to FX fees every time.

- Active Funds & Pensions: Hargreaves Lansdown (Premium service and research, though be wary of the new £150 share fee cap). Personally, I find the 2026 HL fee structure too steep for my larger pots. I have already moved my GIA to Trading 212 and am currently transferring my SIPP to Freetrade to avoid the new £150 share fee cap. However, I still keep a small ‘Fund & Share’ account there because their data on ex-dividend dates and FTSE risers remains superior to the newer apps.

Important Reminder: FSCS Protection

Regardless of which platform you choose, your investments are covered up to £85,000 per person by the Financial Services Compensation Scheme (FSCS) if the platform goes bust. This does not cover you if your investments simply go down in value.

While choosing the right platform is the first step, building a resilient portfolio requires smart diversification. Beyond just picking the right stocks, many UK investors are now balancing their equity holdings with precious metals to hedge against market volatility. If you’re considering this, check out our deep dives into buying gold and investing in silver in 2026 to see which metal suits your risk profile.

The 2026 Switching Guide: How to Move Without Fees

Moving your portfolio is no longer the expensive, paperwork-heavy nightmare it used to be. Most major UK brokers have abolished “exit fees” (the cost per holding to leave) to meet regulatory pressure.

Check Your “Exit Cost”

- Hargreaves Lansdown: As of 2026, HL is free to leave. They no longer charge the historical £25-per-line exit fee or account closure fees.

- Interactive Investor (ii): Most transfers are now free, though you should verify if you have “Share Certificates” or “Paper Deeds,” which still carry a £35 admin fee.

- AJ Bell: Generally free for digital transfers, but always check for “discretionary” charges on complex assets.

Choose Your Transfer Method

| Method | Best For… | The Catch |

| In-Specie (Stock) | Avoiding “Time out of Market.” You keep your exact shares. | Only works if the new broker supports that specific stock/ETF. |

| Cash Transfer | Switching to a broker that doesn’t support your current funds. | You are out of the market for 1–3 weeks; you might miss a market rally. |

The Fractional Share Trap: You cannot transfer fractional shares (e.g., 0.5 shares of Apple). These will always be sold to cash by your old broker before the move.

Broker-Specific Tips (2026 Update)

Moving to Trading 212

- The “Fund” Issue: Trading 212 supports Stocks and ETFs, but it does not support Mutual Funds (OEICs) like the popular Vanguard LifeStrategy or Lindsell Train funds. If you hold these at HL, you must sell them to cash before transferring.

- Incentives: Check the “Promotions” tab in the app. In early 2026, T212 often offers a “Transfer Bonus” or free fractional shares for ISA consolidations.

Moving to Interactive Brokers (IBKR)

- The “Pro” Advantage: IBKR is the best for In-Specie transfers of international stocks. Their “ACATS” and “FOP” systems are faster than the standard UK manual transfer.

- ISA Fees: Remember that while IBKR has no “custody fee” for large portfolios, they have a £3/month minimum fee for ISAs. If your portfolio is under £10k, Trading 212 is cheaper.

Moving to Interactive Investor (ii)

- The “Bundle” Win: As of Feb 2026, ii’s Core, Plus, and Premium plans now bundle the ISA, SIPP, and Trading Account into one monthly fee. You no longer pay extra for a pension wrapper.

- Free Trades: The Plus and Premium plans include one or two free trades per month, which can offset the monthly subscription cost if you are an active investor.

Moving to Freetrade

- The “Basic” Revolution: In late January 2026, Freetrade made their SIPP and ISA free on the ‘Basic’ plan. You no longer need the £11.99/mo subscription just to hold a pension.

- In-Specie Limits: While Freetrade supports “In-Specie” (moving stocks without selling), they cannot hold every complex instrument. Always check their “Stock Universe” list before initiating a transfer to avoid forced liquidations.

Moving to InvestEngine

- ETF-Only Zone: InvestEngine only supports ETFs. If you are moving from a broker like HL or ii where you hold individual stocks (like MSFT or BP), you must sell them to cash before the transfer can complete.

- Automation Edge: Use the “One-Click Rebalancing” tool immediately after your transfer completes to automatically spread your transferred cash across your new target portfolio.

The Golden Rule of ISA Transfers

Never withdraw the money yourself. If you sell your shares and move the cash to your bank account, you lose that year’s ISA tax-free allowance forever. You must initiate the transfer from within the new broker’s app (Trading 212 or IBKR) and let them pull the funds from your old provider.

📝 Summary Checklist

- Open the new account (T212 or IBKR) but don’t fund it yet.

- Identify “Unsupported” Assets: Sell any mutual funds (OEICs) or fractional shares to cash in your old account.

- Initiate “Portfolio Transfer” in the new app. You’ll need your old account number (found on your HL or ii statement).

- Wait 2–4 weeks: The brokers handle the communication. Your old account will eventually show a zero balance and close automatically.

🙋 Frequently Asked Questions (FAQ)

1. Is Interactive Brokers or Trading 212 better for US shares?

If you are making large trades (over £5,000) or trading frequently, Interactive Brokers is usually cheaper due to its industry-low 0.03% FX fee. For smaller, casual investors or those who want fractional shares, Trading 212 is better because it has no monthly fees and a simple interface.

2. Can I buy US ETFs like VOO or QQQ in the UK?

Technically, no. Due to UK “UCITS” regulations, retail investors cannot buy US-domiciled ETFs directly. However, you can buy UK-reporting versions that track the exact same indexes, such as VUSA (for the S&P 500) or EQQQ (for the Nasdaq 100).

3. How do I avoid the 30% US dividend tax?

You must complete a W-8BEN form through your broker. This notifies the IRS that you are a UK resident, which reduces the “withholding tax” on your US dividends from 30% down to 15%. Most modern UK apps handle this digitally during sign-up.

4. Are my investments safe if a platform goes bust?

Most major UK platforms are regulated by the FCA and covered by the FSCS. However, the protection limits depend on whether you are holding cash or assets:

Market Losses: As always, the FSCS does not protect you if your stocks simply go down in value. That is a market risk, not a platform failure risk.

Cash (up to £120,000): If your platform holds your uninvested cash in a UK-regulated bank account and that bank or the platform fails, you are now protected up to £120,000 (increased from £85,000 in late 2025).

Investments (up to £85,000): If the platform fails and your invested assets (stocks/ETFs) are missing or mishandled, the FSCS covers you up to £85,000 per person, per firm.

5. Does it cost money to switch ISA providers in 2026?

In 2026, most major UK brokers (including HL, AJ Bell, and ii) have abolished exit fees. While it is usually free to leave, you should check if your old broker charges a “paperwork fee” for manual transfers of physical share certificates.