Last Updated: 22 February 2026

Key Takeaways

- UPDATE: 22 February 2026

- Price Action: Bitcoin is currently consolidating near £50,300 after a volatile start to the month.

- Bitcoin has seen a 20% drawdown in early 2026 (trading near £50,000), European ETF inflows have remained positive, suggesting institutional resilience.

- The Deadline: On 6 April 2026, Bitcoin/Ether ETNs will be removed from standard Stocks & Shares ISAs.

- The Forced Sale: Major brokers (T212, AJ Bell) will likely sell your holdings to cash if you don’t act.

- The Choice: Move to a General Investment Account (GIA) for security and FSCS protection, or transfer to an Innovative Finance ISA (IFISA) to keep gains 100% tax-free at higher risk. WARNING: IFISA has no FSCS protection. In a “Black Swan” event where a platform collapses, you could lose 100% of your capital regardless of how well Bitcoin is performing.

In this Guide

Since the FCA lifted the retail ban on Cryptoasset Exchange Traded Notes (cETNs) in October 2025, UK investors have flocked to these products. However, a major tax-year transition on 6 April 2026 means the “buy and forget” strategy in your Stocks & Shares ISA is about to change.

Why Bitcoin?

Bitcoin is often dubbed “Digital Gold” due to its fixed supply of 21 million coins. In 2024 and 2025, we saw values surge—hitting peaks near £90,000 in late 2025—driven by institutional adoption and US regulatory progress.

Warning: Bitcoin is purely speculative. It has no earnings or dividends. History is littered with “crypto winters”:

- 2021/22: A drop from ~£50k to ~£13k.

- Early 2026: A recent “flash crash” saw prices retreat from £90k towards £50k in weeks.

- The Bottom Line: Never invest more than you can afford to lose. A 10% daily swing is a “quiet Tuesday” in crypto. Most investors limit crypto exposure to 1%–5% of their total portfolio.

Coinbase vs. ETNs: The Fee & Tax Trap

Traditionally, you would buy on an exchange like Coinbase.

- The Fee Problem: Buying £100 of Bitcoin on a retail exchange can cost 1.5% to 4% in fees. For small, recurring buys, these fees “eat” your future growth before you even start.

- The Tax Killer: Outside an ISA, you only have a £3,000 Capital Gains Tax (CGT) allowance. If Bitcoin doubles, a modest investment can quickly land you with a tax bill of 18%–24% on your profits.

The Democratisation of Crypto ETNs

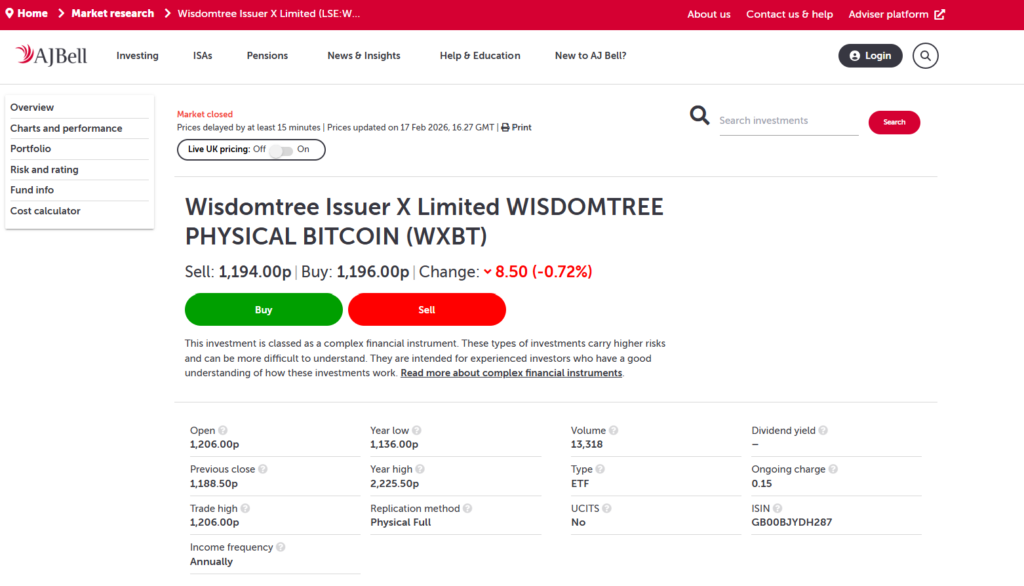

ETNs have changed the rules of the game. You can now buy fractional amounts (even £10 worth) with management fees as low as 0.25%. Tickers like IB1T (BlackRock) or WXBT (Wisdomtree) are physically backed, meaning the provider holds the actual Bitcoin in secure “cold storage.”

Below are the primary “physically backed” tickers available on the London Stock Exchange in GBP. At present you can buy IB1T within an ISA on platforms such as Trading 212. AJ Bell offers WXBT.

| Ticker | Instrument Name | Issuer | Management Fee (TER) |

| IB1T | iShares Bitcoin ETP | BlackRock | 0.15%, 0.25% from 2027 |

| WXBT | WisdomTree Physical Bitcoin | WisdomTree | 0.15% |

How to Buy: The “Approval” Hurdle

Using Trading 212 or AJ Bell as an example, you cannot buy immediately. You must complete three FCA-mandated steps:

You must complete these three FCA-mandated steps in order:

- Restricted Investor Declaration: You must declare that you are a “Restricted Investor,” meaning you will not invest more than 10% of your net assets into high risk investments (like crypto ETNs).

- Appropriateness Test: A short multiple-choice quiz. You need to demonstrate that you understand ETNs and investing in crypto, with no FSCS protection on the asset itself.

- The 24-Hour “Cooling Off” Period: Once you pass the test, the app will legally lock you out for 24 hours. You cannot skip this. It is designed to prevent “impulse buying.”

- After the 24 hours have passed, return to the ticker (e.g., IB1T). You will be asked to confirm one last time that you still wish to proceed. Once you hit Confirm, the “Buy” button will be unlocked for all crypto ETNs on the platform.

The April 6th Deadline: Why You Must Act

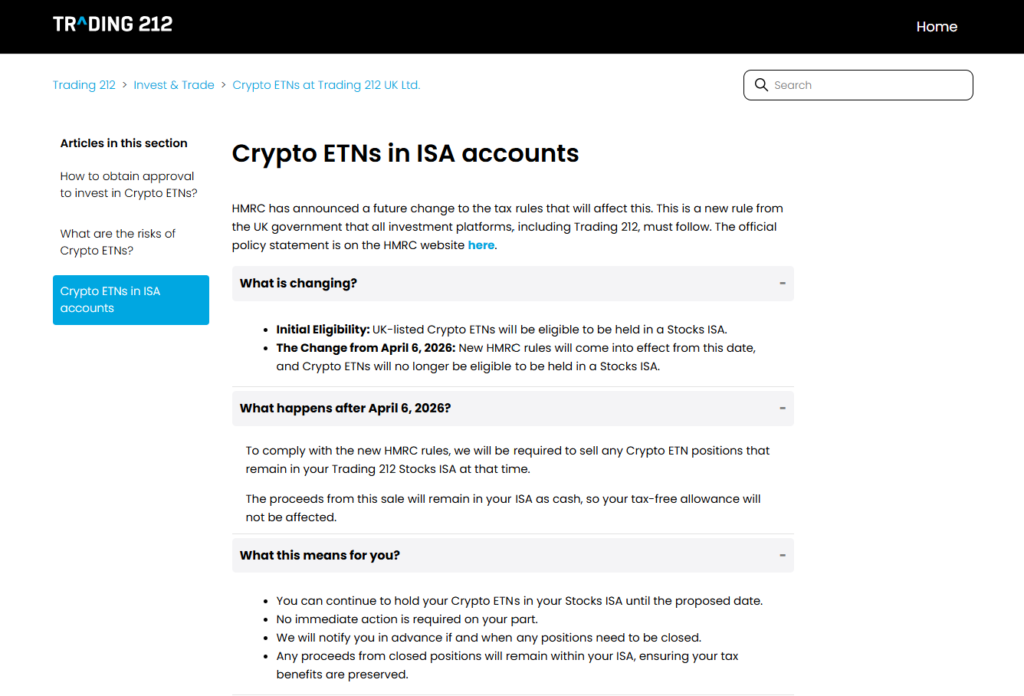

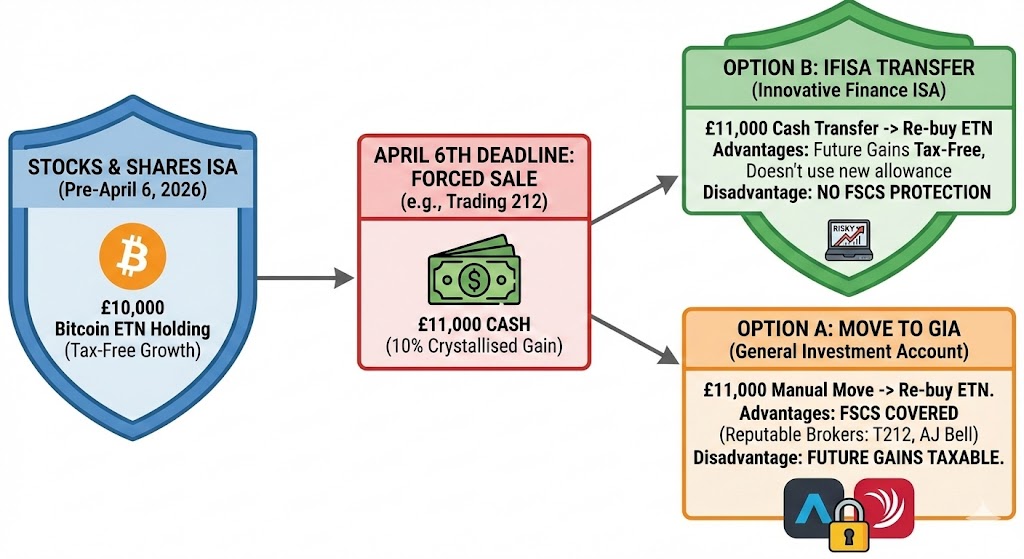

HMRC has ruled that from 6 April 2026, Crypto ETNs are no longer eligible for a standard Stocks & Shares ISA. They are being moved to the Innovative Finance ISA (IFISA). Most mainstream brokers (Vanguard, Trading 212, AJ Bell) do not offer an IFISA. If your broker doesn’t launch an IFISA by April 2026, they will be forced to liquidate your holdings to cash. You have two main choices

Option 1: The “GIA” Move (Simple but Taxable)

You can move your holdings out of the ISA and into your General Investment Account (GIA).

- The Pro: You keep your Bitcoin. You don’t have to deal with complex IFISA providers.

- The Con: You lose your tax-free status. Any future gains will be subject to Capital Gains Tax (CGT) once you exceed your annual allowance (currently £3,000).

Option 2: The IFISA Transfer (Tax-Free but Complex)

You transfer your ISA to a specialized provider that supports the IFISA.

- The Pro: Your gains remain 100% tax-free.

- The Con: IFISAs have £0 FSCS protection. If the platform fails, your money is gone. Many investors find this risk too high for the tax saving.

Trading 212 has stated that after 6 April 2026 – “…we will be required to sell any Crypto ETN positions that remain in your Trading 212 Stocks ISA at that time.”

What about Ether (ETH) ETNs?

Bitcoin isn’t alone. Ether ETNs (like VETH or ETHW) fall under the exact same HMRC axe.

- April 6th Deadline: Both Bitcoin and Ether ETNs will be “evicted” from the Stocks & Shares ISA on the same day.

- Staking Warning: Be careful—some Ether ETNs offer “Staking Rewards.” HMRC’s view on whether these rewards are “Interest” or “Capital Gains” is still evolving. Stick to Physically Backed (Non-Staking) notes for the cleanest tax treatment.

Transfer Out from ISA: GIA vs. IFISA

Most mainstream UK platforms—including Hargreaves Lansdown, AJ Bell, and Trading 212—have been clear: they do not currently plan to launch an Innovative Finance ISA (IFISA). Because Bitcoin ETNs are being “evicted” from the Stocks & Shares ISA on 6 April 2026, these brokers will be required to remove the assets from your tax-free wrapper.

Unless a last-minute regulatory U-turn occurs, you generally face two paths to maintain your Bitcoin exposure:

Path 1: The General Investment Account (GIA) – The Safety Play

Most investors will likely choose to move their holdings into their broker’s General Investment Account (GIA).

- The Process: Your broker sells your ETNs for cash within the ISA (crystallising your gains tax-free up to that point). You then move that cash to your GIA and re-buy the same ticker

- The Advantage: You stay with a reputable, familiar broker. Your funds remain under FSCS oversight for cash and benefit from established institutional custody.

- The Trade-off: Any future growth is taxable. You lose the “tax shield,” and future gains above your annual allowance (currently £3,000) will incur Capital Gains Tax (CGT).

Path 2: The IFISA Transfer – The Tax-Free Play

To keep all future gains 100% tax-free, you must move the funds to a provider that specifically offers an IFISA.

The Trade-off: Most IFISA providers are specialized fintechs (like Crowd2Fund). Unlike major banks, these platforms do not carry FSCS protection. If the platform itself fails, your capital is not guaranteed by the government. You must perform a formal Cash Transfer. Your current broker sells the ETN, and the cash is sent directly to the new IFISA manager. You then re-buy the ETN within that new tax-protected wrapper.

The Advantage: You maintain tax-free status on all future growth. Crucially, because it is a transfer, it does not use up your fresh £20,000 ISA allowance.

Current 2026 IFISA Options for Crypto ETNs:

- Crowd2Fund: One of the few platforms actively marketing a “Crypto-Ready” IFISA. They are building the tech to hold LSE-listed digital notes.

- The “Wait and See” Contenders: Rumors suggest Freetrade or Saxo may launch an IFISA before the deadline to “scoop up” all the Trading 212 refugees. If they do, they will support “In-Specie” transfers, which is the holy grail.

The “One ISA” Myth: Transfer your ETN Without Touching Your Allowance

You can hold a Stocks ISA, an IFISA, and a Cash ISA simultaneously, as long as your new contributions don’t exceed £20,000.

The Golden Rule: Always use a Transfer Form. If you “Withdraw” the money to your bank account, it loses its tax-free status and counts against your £20k limit if you try to put it back in.

How to Handle the Transfer to an IFISA

This is the most critical part of the 2026 Bitcoin ETN transition. Moving money you already have in an ISA is a Transfer, not a Contribution.

The £50,000 Hypothetical Case Study: Imagine you have £50,000 in Bitcoin ETNs within your Trading 212 ISA.

- The Forced Sale: T212 sells your ETNs for cash on April 6th. You now have £50,000 in cash sitting in the T212 “wrapper.”

- The Rescue: You open an IFISA with a provider like Crowd2Fund and request a formal ISA Transfer.

- The Result: The £50k moves to the new provider. This uses £0 of your 2026 allowance.

- The Bonus: You can still deposit a fresh £20,000 into your ISA during the year. You now have £70,000 protected from HMRC.

The IFISA Risks: What They Don’t Tell You

Investing in Bitcoin ETNs via an IFISA is a high conviction move. While the tax benefits are massive, you are stepping outside the traditional safety net of UK banking. For many, moving to a GIA (General Investment Account) with a major broker is actually the safer, more logical path.

- No FSCS Protection Unlike your cash savings (protected up to £120,000 in 2026) or even your standard stocks (protected up to £85,000 if a broker fails), the Bitcoin investment in an IFISA has zero protection. If your IFISA provider goes bust, or if the Bitcoin ETN issuer (like BlackRock) defaults, the FSCS will not step in to bail you out. You are 100% on your own. By moving your Bitcoin to a GIA with a reputable broker like AJ Bell or Trading 212, you remain within the FSCS framework for your cash and the broker’s regulatory custody for your assets. For many, the peace of mind is worth the potential tax bill.

- Platform Risk. Because IFISAs are a “niche” product (only about 17,000 exist compared to 3.8 million Stocks ISAs), the platforms are often smaller fintechs. If thousands of people try to sell their Bitcoin ETNs at once during a crash, a small IFISA provider might struggle with liquidity. You could find yourself unable to sell or withdraw your cash for days or even weeks. Unlike major brokers, where you can sell in seconds, some IFISAs require another buyer to “take over” your position before you can exit. Major brokers often have more robust trading desks to handle high volume ETN trades than specialized IFISA fintechs.

| Asset Type | Wrapper | Risk Level | FSCS Protection | The Bottom Line |

| Cash Savings | Cash ISA | Low | £120,000 | Maximum Security but low growth, value eroded by inflation |

| ETFs e.g. VUSA, VUKE | Stocks ISA | Low/Med | £85,000* | Stable, protected income. |

| Bitcoin ETN | GIA | High | £85,000* | Volatile, but held by major, protected brokers. |

| Bitcoin ETN | IFISA | Extreme | £0 | Tax-free, but you are 100% on your own. |

*Protection applies to broker failure/cash, not the value of the investment itself.

The “CLARITY” Act: Why the US matters to UK Investors

The US Digital Asset Market Clarity Act (2025) is the “North Star” for UK regulators. While it passed the House in 2025, the Senate Banking Committee delayed the bill on 14 January 2026.

- The “Commodity” Win: If the US officially classifies Bitcoin and Ether as commodities (rather than securities), the FCA is expected to follow suit.

- The Result: This could eventually lead to the UK allowing these ETNs back into the Stocks & Shares ISA by 2027 or 2028.

Summary & FAQs

Q: Will I lose my ISA tax-free status if T212 sells my Bitcoin? A: No, as long as the money stays in the ISA as cash. However, you won’t be able to re-buy Bitcoin on T212. You must transfer that cash to a GIA or IFISA to buy back in.

Q: Is it better to move to a GIA or an IFISA? A: It depends on your priority. A GIA at a major broker (like Trading 212 or AJ Bell) offers high security and FSCS protection, but your future gains are taxable. An IFISA keeps your gains tax-free but generally offers zero FSCS protection and carries higher platform risk. For smaller holdings, the GIA is often the more sensible “middle ground.”

Q: How long does a transfer take? A: Typically 15 to 30 days. You will be “out of the market” during this time, so plan for price volatility.

Q: Can I put £20k in my Stocks ISA and another £20k in my IFISA? A: No. Your total new money across all ISAs is capped at £20,000 per year. You can, however, transfer unlimited amounts of old ISA money.