- The Inflation Reality: Since 2022, the purchasing power of cash held in standard bank accounts has eroded by over 20%.

- Risk Parameters: A robust portfolio should prioritise low cost index ETFs and tax efficient wrappers. Individual share picking is higher risk and requires the temperament to withstand higher price volatility. All investing requires a longer term term horizon of three to five years to increase the chances of good, positive returns

- Tax Deadlines: We are within the final 50 days of the tax year; initiating “Bed and ISA” transfers now is critical to avoid the March administrative bottleneck.

- Geopolitical Outlook: Markets currently favour a “divided government” in the US midterms to provide stability against ongoing trade policy uncertainty.

Protecting capital in 2026 requires a deliberate approach. These insights are drawn from twenty years of personal experience in the UK markets and are designed for those managing their own portfolios.

I began investing shortly after the 2008 financial crisis. I vividly recall the FTSE 100 languishing below 4,000 points and NatWest shares hitting lows of 11p. It seemed an obvious moment to secure assets that were too cheap to ignore. It was, of course, a period of high risk, and I was still learning the ropes. At that time, share dealing was a cumbersome process involving high fees and waiting for security codes to arrive by post. Today, an account can be opened in minutes.

- Comparing the Best UK Investment Platforms for 2026: An objective review of Trading 212, Interactive Brokers, and the recent fee overhauls at Hargreaves Lansdown.

- The 2026 Guide to UK Dividend and Capital Gains Tax: With thresholds tightening, understanding “Bed and ISA” transfers and Gilt ladders is essential for protecting your net return

However, ease of access has arguably increased the risk of poor decision making. We now see a culture of “meme” stocks and online forums where significant accounts are zeroed out by reckless speculation. Witnessing this is humbling. I now follow a personal rule: I never buy an individual share unless I can answer two questions:

- Time Horizon: Do I need this capital within the next two to three years? If the answer is yes, it does not belong in individual shares, invest in index ETFs with caution

- Resilience: If the share price drops by 50% tomorrow, will I sleep well? If I cannot stomach that volatility, I should not be picking shares.

I learned these lessons the hard way. There is no reliable get rich quick scheme. The core of my portfolio remains in ETFs tracking the S&P 500, the FTSE 100, and global income producing stocks. When I do select individual companies, I focus on those with robust financials, growing free cash flow, and a genuine “moat” that protects their business—such as Google or Amazon. Concentrating solely on a single sector, such as Tech or AI, creates a portfolio that is vulnerable to specific downturns. Similarly, over-allocating to cyclical sectors like mining or oil carries unique dangers.

- Top 2026 ETFs for UK Investors: A selection of the best Sterling denominated trackers for those seeking long term capital growth.

- Accessing US Markets from the UK: How to manage currency conversion fees, and choose the best platforms for investing in the US.

The BP Case Study

BP serves as a sobering example of how quickly a “Blue Chip” can falter. In April 2010, BP traded near all time highs of around £6 before the Deepwater Horizon disaster caused the price to crater, more than halving within months. The company has never truly regained its former standing, having sold billions in assets to cover fines.

Following years of navigating crises, management pivoted in 2020 towards a strategy that moved away from core oil and gas exploration into renewables with unproven returns. The market is efficient at punishing perceived hubris. The share price struggled, and leadership has remained in flux. With a third CEO in less than three years taking the helm on 1 April 2026, the question remains: is BP a turnaround opportunity or a company still hampered by its past strategic pivots? When compared to peers like Shell or ExxonMobil, the unique value proposition is increasingly difficult to define.

The market is watching to see if the new BP CEO steers BP back towards oil and away from the contested renewables pivot. The penalty for failing to impress investors could be very painful to the share price as the expectations are very high.

The Cost of Holding Cash

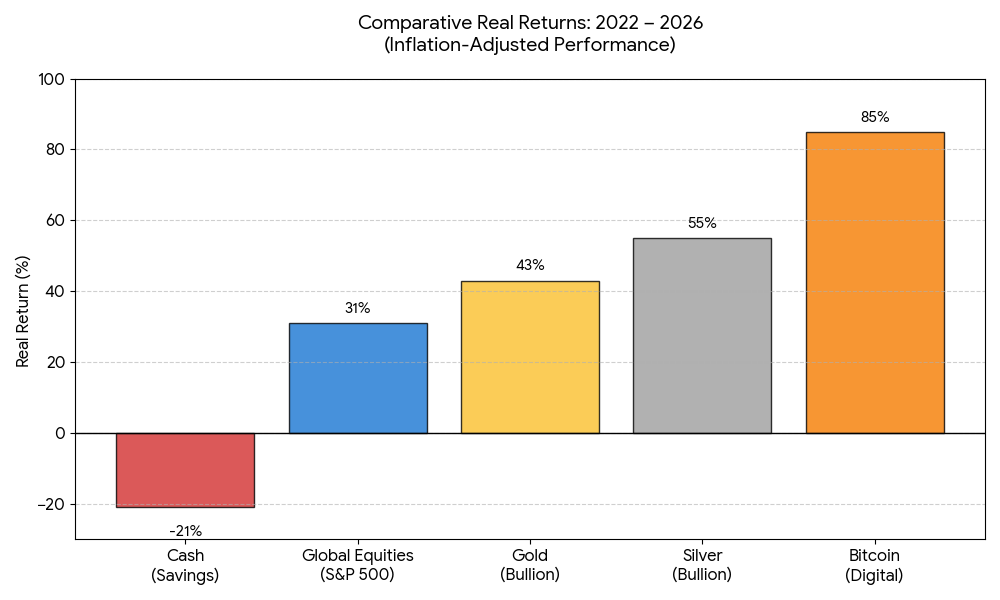

Investing in the stock markets is risky, but keeping cash in the bank and avoiding any investing due to the fear of losing money is, in my view, just as risky. Inflation remains a quiet but persistent challenge. If you held £10,000 in a standard bank account in January 2022, by early 2026 the real value of that capital has significantly diminished.

While the nominal balance remains unchanged, its purchasing power has eroded by approximately 21% over the last four years. Effectively, your £10,000 now only buys what £7,893 would have purchased at the start of 2022. These calculations use average inflation data from 2022 through to 2025 from the Office for National Statistics.

Comparative Returns of Various Assets (2022– Feb 2026)

Other asset classes such as investing in the S&P 500 Index (e.g. VUSA ETF) or Gold would have netted you higher returns. Silver and Bitcoin would have been stellar performers – but be warned that these are very volatile asset classes and investing in them requires long terms horizons, the ability to stomach extreme price action and attention to unique pricing concepts such as the GSR.

- Gold as a Currency Hedge in 2026: Why physical gold remains a vital “Plan B” in a period of fiscal uncertainty.

- The Outlook for Silver: Industrial and Monetary Trends: Evaluating the supply deficit and the potential for a rerating in silver prices.

- Digital Assets in a UK Tax Wrapper: Navigating the new Bitcoin ETN options and their eligibility for ISAs and SIPPs.

The data suggests that for long term wealth preservation, a move towards tax efficient, diversified assets is no longer optional. You can see from the above interactive chart that the FTSE 100 or S&P500 have both provided yields well above the rate of inflation – but also note the falls in the index during particular years – especially during the 2020-2021 Covid crisis! This highlights that investing in the markets always requires a longer term horizon for the bst returns.

About this Site

This site is a personal hobby. I work in the City and have a deep interest in investing in stocks and understanding how economies work. I do not claim to be an investing guru – however, my experiences, successes, and many failures have taught me valuable lessons that I have decided to document as part of my personal growth. If these guides help someone else make an informed investing decision, then that is a welcome bonus.

Core Guides for 2026

Below are my primary articles, structured to help you navigate the current landscape. Each guide is updated for the 2026/27 tax year with a focus on minimising costs and maximising tax efficiency.

Platforms and Tax Efficiency

The most common mistake is overpaying for the privilege of investing. These guides focus on the infrastructure of your portfolio.

- Comparing the Best UK Investment Platforms for 2026: An objective review of Trading 212, Interactive Brokers, and the recent fee overhauls at Hargreaves Lansdown.

- The 2026 Guide to UK Dividend and Capital Gains Tax: With thresholds tightening, understanding “Bed and ISA” transfers and Gilts is essential for protecting your net returns.

Global Growth and Equities

Building a diversified core using low cost funds and selected individual companies.

- Top 2026 ETFs for UK Investors: A selection of the best Sterling denominated trackers for those seeking long term capital growth.

- Accessing US Markets from the UK: How to manage currency conversion fees and picking the best platforms for investing in US shares.

Alternative Assets and Hedges

Insurance against a weakening Pound and systemic volatility.

Digital Assets in a UK Tax Wrapper: Navigating the new Bitcoin ETN options and their eligibility for ISAs and SIPPs.

Gold as a Currency Hedge in 2026: Why physical gold remains a vital “Plan B” in a period of fiscal uncertainty.

The Outlook for Silver: Industrial and Monetary Trends: Evaluating the supply deficit and the potential for a rerating in silver prices.

Market Pulse: 2H February 2026

- US Mid Term Outlook: As we look towards the 2026 mid term elections, polling suggests a likely shift towards the Democrats regaining control of the House. With Republican retirements at a five year high, the ‘Blue Wave’ narrative is gaining significant momentum in the City’s US desks. For equity markets, a divided government in Washington often provides a period of legislative stability. Many investors prefer this predictability, as it reduces the likelihood of radical policy changes, though the ongoing uncertainty surrounding the trade actions of President Donald Trump remains a factor that could introduce sudden volatility.

- FTSE 100 Record Highs: Following the US Supreme Court ruling on 20 February against sweeping tariffs, the FTSE 100 hit a new intraday peak of 10,745. Export heavy “Blue Chips” such as Diageo saw a significant relief rally as tariff fears eased.

- Inflation Update: The latest ONS data shows CPI inflation has cooled to 3.0%. This has increased expectations that the Bank of England may begin cutting the Base Rate as early as the March meeting, potentially shifting the appeal of cash savings back towards equities and Gilts.

- Tax Year End: We are now inside the 50 day window before the 5 April tax deadline. If you have remaining ISA or SIPP allowances, ensure your transfers are initiated by mid March to avoid the inevitable processing delays.